So far, I've been doing a series on money and banking, monetary policy/quantitative easing (QE), and the impacts of QE. I'm kind of continuing the series (if you think this post is about continuing the series). In modern macroeconomics, students are taught IS/LM.

Before I touch on the basics of IS/LM and go into why it's not a very good macro model, I'll go through the history. Contrary to popular opinion, IS/LM was not a model developed by Keynes. IS/LM was developed by John Hicks in a paper titled Mr. Keynes and the Classics. IS/LM was a model developed by Hicks as it was Hicks' interpretation of Keynes' General Theory of Employment, Interest, and Money. However, Keynes explicitly rejects IS/LM in his paper, Alternative Theories of the Rate of Interest. Ironically, IS/LM is still taught by professors in economics and is portrayed as "Keynesian" when Keynes didn't have a very high opinion on the model. Here's a quote from Keynes talking about the "alternative theory" Keynes refers to in the quote below is the IS/LM model laid out by Hicks, Ohlin, and other economists.

Before I touch on the basics of IS/LM and go into why it's not a very good macro model, I'll go through the history. Contrary to popular opinion, IS/LM was not a model developed by Keynes. IS/LM was developed by John Hicks in a paper titled Mr. Keynes and the Classics. IS/LM was a model developed by Hicks as it was Hicks' interpretation of Keynes' General Theory of Employment, Interest, and Money. However, Keynes explicitly rejects IS/LM in his paper, Alternative Theories of the Rate of Interest. Ironically, IS/LM is still taught by professors in economics and is portrayed as "Keynesian" when Keynes didn't have a very high opinion on the model. Here's a quote from Keynes talking about the "alternative theory" Keynes refers to in the quote below is the IS/LM model laid out by Hicks, Ohlin, and other economists.

The alternative theory … makes it to depend … on the demand and supply of credit or, alternatively (meaning the same thing), of loans, at different rates of interest. Some of the writers … believe that my theory is, on the whole, the same as theirs and mainly amounts to expressing it in a somewhat different way. Nevertheless the theories are, I believe, radically opposed to one another.

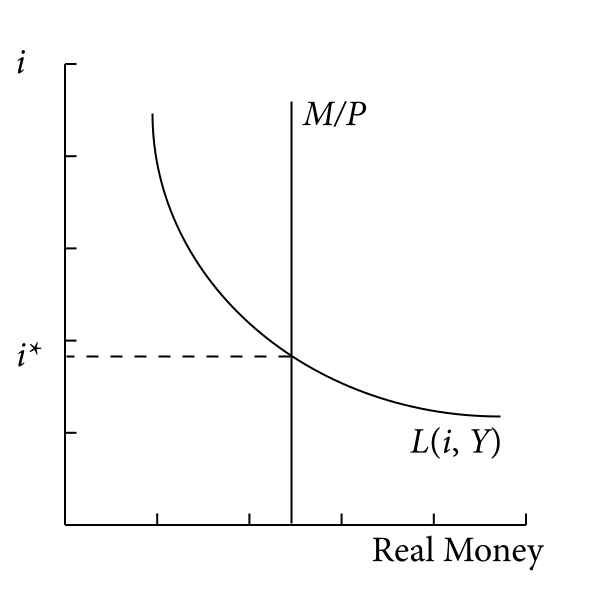

IS/LM is a common method designed to teach economics students about the impact that shifting interest rates has on macroeconomies. IS/LM is initially derived by (correctly) assuming that the central banks shift the rate of interest by altering the supply of base money (or reserves). IS/LM also assumes that there's a magical stock of savings that get lent out by banks and get magically turned into loans. There are two curves that are drawn: the investment savings (IS) curve and the liquidity preference-money supply (LM) curve. The IS curve comes from the identity that investment and savings are equal. The IS curve is assumed to be downward sloping where an increase in the rate of interest leads to a drop in output and vice versa. The LM curve is derived from a (correct) graph (see the left chart below) that shows the relationship between the short term money market rate of interest as being set by the supply of base money and a downward sloping curve that represents the demand for base money. Then, the relationship between the rate of interest and the nominal income can be derived--which ends up being an upward sloping curve. The intersections between the two curves then determines both the rate of interest and the output level (see the chart on the right).

One of the primary problems with IS/LM is that it starts with the assumption that savings get lent out. In fact, savings do not get lent out. Loans always have, and always will, create deposits. There is an accounting identity that tells us S=I for a closed economy (and for the world economy--because the world is closed). However, S=I is an accounting identity derived from the fact that Y=C+I+NX=C+S which implies S=I+NX. In a closed economy, there are no net exports which tells us that S=I. It is a mistake to say that S=I because savings get lent out. If we use the framework of loans creating deposits, we end up realizing that the creation of debt creates money and investment is driven, not by an existing stock of savings that banks keep around, but by newly created money. This investment has to go to someone and ends up as someone else's income. We must remember that savings is, by definition, income not consumed. So investment actually creates savings. IS/LM makes the mistake of assuming savings creates investment.

Another mistake of IS/LM is that there's absolutely no theory of the yield curve. IS/LM gives students the impression that when the central bank lowers short term interest rates, output goes up because people start hold less securities and more money gets lent out. It can give the impression to students that lower interest rates mean higher inflation. In IS/LM, there is absolutely no theory about the yield curve or the rate of exchange. A better approach would be to talk about the present value effect and the impact of short term yields on asset prices. When central banks lower short term interest rates, they do so by expanding their balance sheets. They can buy a Treasury bill by issuing new dollars that either serve as bank reserves or show up as deposits on a dealer balance sheet. This means that not only do short term interest rates fall, but you've also shifted the asset portfolio of the private sector. The private sector will rebalance their portfolios, usually by buying assets of some kind with the extra cash they hold. In other words, central banks changing short term interest rates works by changing the liquidity structure of the private sector which forces the private sector to rebalance their portfolios. Another effect, as stated earlier, by having central banks set the short term rate of interest is the present value effect. The real value of an asset is the NPV of all the future expected cash flows and the real value or productivity of an asset like a factory will not change. However, changing the short term interest rate changes the future "safe" cash flow possible. Asset markets will naturally adjust such that lower short term interest rates usually mean higher asset prices and vice-versa. The reason lower short term interest rates are usually stimulative is because of the impact of the portfolio rebalancing effect and the present value effect--both of which put upward pressure on asset prices. The upward pressure on asset prices causes people to feel richer and consume more of their income (or take out more loans) today.

A third mistake of IS/LM is to completely ignore the differences between short term and long term rates. IS/LM provides no theory for the shape of the yield curve, but the shape of the yield curve is extremely important in determining what happens. There's a common mistake that's been made by several economists (including many heterodox economists) which is that a central bank that comes in to buy long term bonds reduces long term interest rates. The main point here is that having a central bank buy more securities and expand the base money supply doesn't mean that long term rates will move the same way as short term rates--particularly at the zero lower bound.

IS/LM also makes another critical error on the interest rate. The short term money market rate of interest is not the equilibrium rate where the supply of loanable funds meets the demand for loans. Instead, the short term money market rate of interest is simply the price of liquidity. Every single business MUST meet its cash commitments or otherwise it goes bust (liquidity constraint). The short term interest rate is the price at which any firm can obtain liquidity in order to make its payments and prevent itself from going bust. The bank doesn't really have a choice to acquire liquidity if the bank doesn't already have the liquidity on hand. The bank MUST acquire the liquidity and make its payments, regardless of the price. In other words, the short term interest rate isn't the equilibrium rate in the loanable funds marketplace. The short term market rate of interest is the price at which firms must obtain liquidity.

IS/LM also makes another critical error on the interest rate. The short term money market rate of interest is not the equilibrium rate where the supply of loanable funds meets the demand for loans. Instead, the short term money market rate of interest is simply the price of liquidity. Every single business MUST meet its cash commitments or otherwise it goes bust (liquidity constraint). The short term interest rate is the price at which any firm can obtain liquidity in order to make its payments and prevent itself from going bust. The bank doesn't really have a choice to acquire liquidity if the bank doesn't already have the liquidity on hand. The bank MUST acquire the liquidity and make its payments, regardless of the price. In other words, the short term interest rate isn't the equilibrium rate in the loanable funds marketplace. The short term market rate of interest is the price at which firms must obtain liquidity.

So far, I've assumed that the economy in question is closed and FX impacts are non-existent. Another problem with IS/LM is that IS/LM completely ignores FX effects and doesn't take into account the supply side structure of an economy. For example, a country that imports lots of food and energy will respond completely differently to reduction in the short term money market rate of interest (or an increase in the monetary base) than a country that's a heavy exporter of raw materials and energy. IS/LM effectively overlooks all of those factors.

Basically, IS/LM is a poor model. Although it gets some of the impacts correct (like not calling hyperinflation when the Fed buys massive amounts of assets at the zero lower bound), the thinking and the flaws in the model begin with its very assumptions. IS/LM is a bad way of getting students to think about economic factors and holds little use, even as a classroom gadget.

Note: I've only discussed what I find to be the most obvious flaws of IS/LM. Many more flaws exist with the model that I haven't covered in this post. How can any model talk about the impact of monetary policy without talking about the movement of asset prices? The reality is that such a model cannot accurately describe how the world works or even come close to doing so.

Basically, IS/LM is a poor model. Although it gets some of the impacts correct (like not calling hyperinflation when the Fed buys massive amounts of assets at the zero lower bound), the thinking and the flaws in the model begin with its very assumptions. IS/LM is a bad way of getting students to think about economic factors and holds little use, even as a classroom gadget.

Note: I've only discussed what I find to be the most obvious flaws of IS/LM. Many more flaws exist with the model that I haven't covered in this post. How can any model talk about the impact of monetary policy without talking about the movement of asset prices? The reality is that such a model cannot accurately describe how the world works or even come close to doing so.

Are you going to refer to the tone in J.R. Hicks's paper in the [I]Journal of Post Keynesian Economics[/I] in this series?

ReplyDeleteProbably not. Maybe. I'm not sure.

DeleteHi,

ReplyDeleteYou have really shared the wonderful post, you blog is also very informative. You have done the great research in this topic. Personal loans